If you hear the term “credit invisible” it means that you may not have credit files with the nationwide credit reporting agencies — Transunion, Experian and Equifax — or that the information that exists on your credit reports is very limited.

Credit invisibility doesn’t only apply to young individuals who haven’t built up their history yet. It can also apply to older individuals who have stopped using credit, or to Americans who live abroad and don’t keep their U.S. credit accounts active.

Lacking Credit History

Credit invisibility can be detrimental for a number of reasons. Lacking credit history can make it difficult or impossible to secure new lines of credit. This means you may not be able to get a loan for the house or car you want, or open a new credit card account. It could also make it more difficult for you to rent an apartment or get hired for a job.

Keep your credit files up-to-date

Stay up to date with your credit standing by checking your report regularly. Consumers may obtain credit reports from Transunion, Experian, and Equifax every twelve months for free. We recommend that you request your reports from the credit bureaus in writing and have them mailed to you. You should enclose two forms of identification, such as a current driver’s license and utility bill, with your request. Once you have your reports, review your information to make sure that all of your information is accurate.

Seek Legal Help

Flitter Milz is a nationally-recognized consumer protection law firm that represents victims of inaccurate credit report listings. Contact us for a free legal evaluation of errors that appear on your report.

Before applying for any new line of credit, it’s good practice to

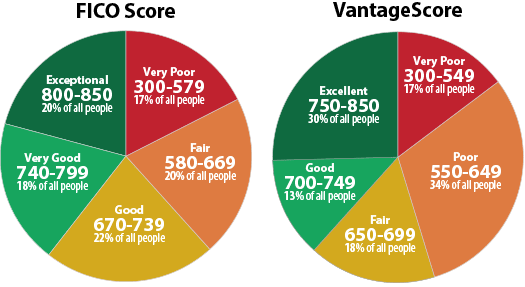

Before applying for any new line of credit, it’s good practice to  However, credit scores that fall in the non-prime (620-679) and subprime (550-619) ranges may not necessarily indicate that you aren’t eligible for a reasonable interest rate. Lenders often use different tiers according to their own business needs to assess creditworthiness.

However, credit scores that fall in the non-prime (620-679) and subprime (550-619) ranges may not necessarily indicate that you aren’t eligible for a reasonable interest rate. Lenders often use different tiers according to their own business needs to assess creditworthiness. Flitter Milz is a consumer protection law firm that pursues matters against lenders, debt collectors and the credit bureaus. If a lender wrongfully repossesses a vehicle, a debt collector is abusive or the credit bureaus report information inaccurately, the consumer may have a lawsuit to pursue. For a no cost legal evaluation,

Flitter Milz is a consumer protection law firm that pursues matters against lenders, debt collectors and the credit bureaus. If a lender wrongfully repossesses a vehicle, a debt collector is abusive or the credit bureaus report information inaccurately, the consumer may have a lawsuit to pursue. For a no cost legal evaluation,

A

A  When you need to secure a loan for the purchase of your new vehicle,

When you need to secure a loan for the purchase of your new vehicle,

Protection from Repossession

Protection from Repossession After a vehicle has been repossessed, the lender is required to send proper notices to the borrower. Shortly after the repossession, the lender will send a letter called a Notice of Intent to Sell Property, which confirms the repossession occurred and details terms for to retrieve the vehicle. If the borrower is not able to meet the terms, the lender may choose to sell the vehicle at an auction or private sale. Once the sale has taken place, the lender will send a second letter called a Deficiency Notice, which informs the borrower of the sale price of the vehicle and any remaining balance due. If the borrower is not notified properly, there may be grounds to file a lawsuit against the lender.

After a vehicle has been repossessed, the lender is required to send proper notices to the borrower. Shortly after the repossession, the lender will send a letter called a Notice of Intent to Sell Property, which confirms the repossession occurred and details terms for to retrieve the vehicle. If the borrower is not able to meet the terms, the lender may choose to sell the vehicle at an auction or private sale. Once the sale has taken place, the lender will send a second letter called a Deficiency Notice, which informs the borrower of the sale price of the vehicle and any remaining balance due. If the borrower is not notified properly, there may be grounds to file a lawsuit against the lender.