Flitter Milz Attorneys meet with JAG officers at local bases to discuss Military Consumer Law

This past summer our attorneys visited Joint Base McGuire-Dix-Lakehurst in New Jersey and Dover Air Force Base in Delaware to educate military lawyers (commonly known as Judge Advocates General or “JAGs”) about common scams targeting servicemembers and how consumer protection laws exist to give our men and women in uniform some measure of relief.

This past summer our attorneys visited Joint Base McGuire-Dix-Lakehurst in New Jersey and Dover Air Force Base in Delaware to educate military lawyers (commonly known as Judge Advocates General or “JAGs”) about common scams targeting servicemembers and how consumer protection laws exist to give our men and women in uniform some measure of relief.

Scams to our Servicemembers

Young and impressionable servicemembers often become targets of scammers. Factors such as reliable pay checks and great military benefits, as well as being subject to sudden deployment and relocation, make servicemembers easy prey for payday lenders, buy-here-pay-here auto dealers, and sub-prime finance companies.

Young and impressionable servicemembers often become targets of scammers. Factors such as reliable pay checks and great military benefits, as well as being subject to sudden deployment and relocation, make servicemembers easy prey for payday lenders, buy-here-pay-here auto dealers, and sub-prime finance companies.

The Law is on your side

Fortunately, the “Military Lending Act” places caps on interest rates to be charged, mandates certain disclosures, and prohibits the use of arbitration clauses in credit agreements. A violating seller can face punitive damages and having to pay the servicemember’s attorney fees.

Fortunately, the “Military Lending Act” places caps on interest rates to be charged, mandates certain disclosures, and prohibits the use of arbitration clauses in credit agreements. A violating seller can face punitive damages and having to pay the servicemember’s attorney fees.

The “Servicemembers Civil Relief Act” or SCRA provides additional protections. It says a creditor may not take a default judgment against an active servicemember. SCRA requires a landlord abide protections for leasing rentals to active military, and empowers courts to stay (or temporarily halt) certain foreclosure and repossession proceedings. The servicemember can also seek damages and their attorney fees for a violation.

The “Servicemembers Civil Relief Act” or SCRA provides additional protections. It says a creditor may not take a default judgment against an active servicemember. SCRA requires a landlord abide protections for leasing rentals to active military, and empowers courts to stay (or temporarily halt) certain foreclosure and repossession proceedings. The servicemember can also seek damages and their attorney fees for a violation.

Consumer Protection Laws for Servicemembers

Of course, all the other consumer protection laws Flitter Milz, PC routinely uses are also available to servicemembers. We have had military clients utilize the Fair Credit Reporting Act (FCRA) to remedy errors on their credit profiles that kept them from getting a promotion or security clearance. Others have used the Fair Debt Collection Practices Act (FDCPA) to stave-off harassing collection attempts and repos. Over all, we have helped thousands of consumers get relief from abusive commercial practices.

Seek Legal Help at No Cost

Flitter Milz is a nationally recognized consumer protection law firm that assists servicemembers who have become victim to credit reporting privacy and accuracy violations, abuse from debt collectors, and vehicle repossessions by aggressive lenders and repo agents.

Flitter Milz is a nationally recognized consumer protection law firm that assists servicemembers who have become victim to credit reporting privacy and accuracy violations, abuse from debt collectors, and vehicle repossessions by aggressive lenders and repo agents.

If you’re a servicemember who has been exposed to unfair, fraudulent or deceptive conduct by a business, CONTACT US for a no cost consultation. We may be able to help.

Pictured above: Attorneys Cary Flitter (center), Andy Milz (left), Jody López-Jacobs (right).

Maybe you aren’t completely sold on solar panels, and simply want more information about switching to solar power. Beware. At this point of the presentation, the salesperson may casually suggest that you submit an application, just to see whether or not you qualify for solar panels. You’ll be offered an iPad or tablet to sign, and be told not to worry because you’ll receive copies of all documents by email.

Maybe you aren’t completely sold on solar panels, and simply want more information about switching to solar power. Beware. At this point of the presentation, the salesperson may casually suggest that you submit an application, just to see whether or not you qualify for solar panels. You’ll be offered an iPad or tablet to sign, and be told not to worry because you’ll receive copies of all documents by email. Placing your signature or initials on an iPad, tablet, or phone may seem easy. However, your electronic signature or initials may be copied and affixed to a contract or other forms that you did not intend.

Placing your signature or initials on an iPad, tablet, or phone may seem easy. However, your electronic signature or initials may be copied and affixed to a contract or other forms that you did not intend. Solar companies rely on financing to make solar panels available to consumers. Credit reports are accessed to evaluate a potential customer’s creditworthiness. The consumer must provide written permission for the solar company to obtain these reports.

Solar companies rely on financing to make solar panels available to consumers. Credit reports are accessed to evaluate a potential customer’s creditworthiness. The consumer must provide written permission for the solar company to obtain these reports. Solar panels will be free.

Solar panels will be free. Many times, the solar panel company may not want to sell you the panels. If you, the buyer, purchases the panels, you would receive the tax credit, not the solar company. If the solar company leases you panels and only promises to sell you the solar power, the solar sales company may receive the tax credit, not you, the homeowner.

Many times, the solar panel company may not want to sell you the panels. If you, the buyer, purchases the panels, you would receive the tax credit, not the solar company. If the solar company leases you panels and only promises to sell you the solar power, the solar sales company may receive the tax credit, not you, the homeowner. Your Neighbors Are Doing It!

Your Neighbors Are Doing It! Flitter Milz is a nationally recognized consumer protection law firm that evaluates solar panel sales matters for potential violation of the consumer protection laws involving fraud, such as forged contracts, identity theft and credit reporting privacy violations.

Flitter Milz is a nationally recognized consumer protection law firm that evaluates solar panel sales matters for potential violation of the consumer protection laws involving fraud, such as forged contracts, identity theft and credit reporting privacy violations.  Understand credit scores and credit reports

Understand credit scores and credit reports What is a credit score?

What is a credit score? credit and obtain copies of his or her credit reports and credit scores.

credit and obtain copies of his or her credit reports and credit scores. Transunion, Experian and Equifax are the three main credit reporting bureaus. These bureaus provide credit reports which list specific information about a consumer’s credit activity and payment history. Lenders use these reports to help determine whether to extend credit or not. As well, other businesses such as insurance companies and utilities, or prospective employers and landlords, may request access to a consumer’s report for use in making decisions about you.

Transunion, Experian and Equifax are the three main credit reporting bureaus. These bureaus provide credit reports which list specific information about a consumer’s credit activity and payment history. Lenders use these reports to help determine whether to extend credit or not. As well, other businesses such as insurance companies and utilities, or prospective employers and landlords, may request access to a consumer’s report for use in making decisions about you.  Do you have errors on your credit reports? Problems getting credit?

Do you have errors on your credit reports? Problems getting credit?

An individual or business may request access to a consumer’s credit file, but they must obtain written permission from the consumer. Often, during the process of applying for credit, interviewing with a prospective employer or landlord, or applying for utilities, there may be a request to access the consumer’s credit file. Many times the credit application will serve as written permission. Other times, a specific document will be presented to the consumer for his or her signature.

An individual or business may request access to a consumer’s credit file, but they must obtain written permission from the consumer. Often, during the process of applying for credit, interviewing with a prospective employer or landlord, or applying for utilities, there may be a request to access the consumer’s credit file. Many times the credit application will serve as written permission. Other times, a specific document will be presented to the consumer for his or her signature. Consumers must

Consumers must

J

J

4. If Inaccurate…Dispute! After obtaining your credit report, if there are errors, you should

4. If Inaccurate…Dispute! After obtaining your credit report, if there are errors, you should  One Dispute Letter Per Error. If you find multiple errors on a credit report, dispute them individually with the bureau. Enclose a copy of the credit report with the error highlighted and your supporting documents. The credit bureaus then have 30 days to respond to your dispute letter.

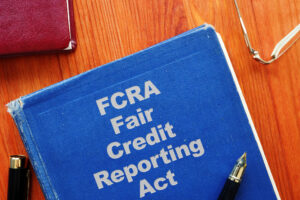

One Dispute Letter Per Error. If you find multiple errors on a credit report, dispute them individually with the bureau. Enclose a copy of the credit report with the error highlighted and your supporting documents. The credit bureaus then have 30 days to respond to your dispute letter. The Fair Credit Reporting Act

The Fair Credit Reporting Act  Flitter Milz, P.C. represents people in consumer credit matters related to credit reporting accuracy and privacy, abusive debt collection contact and vehicle repossessions which stem from a pending divorce or separation.

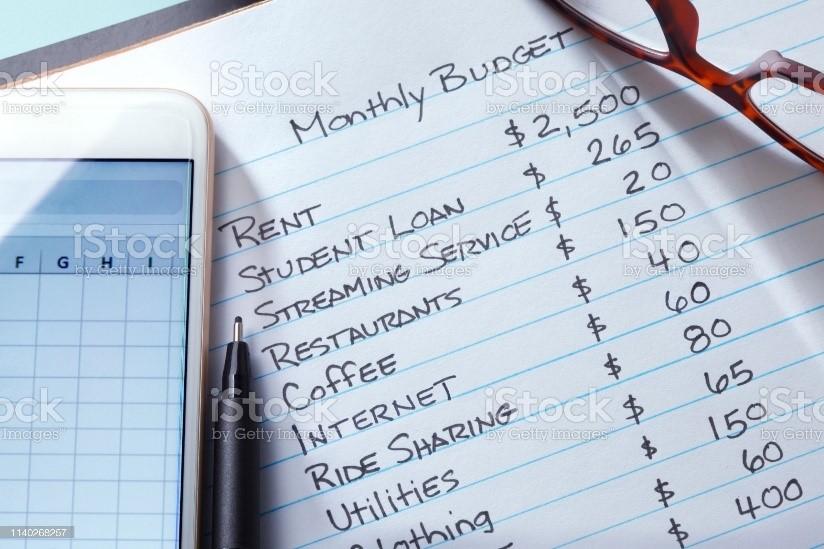

Flitter Milz, P.C. represents people in consumer credit matters related to credit reporting accuracy and privacy, abusive debt collection contact and vehicle repossessions which stem from a pending divorce or separation.  Crafting a household budget is not only necessary to help evaluate spending patterns and measure income versus expenditures, but it also helps to ensure a secure financial future.

Crafting a household budget is not only necessary to help evaluate spending patterns and measure income versus expenditures, but it also helps to ensure a secure financial future. If you know how much money is coming in versus going out each month, it becomes less likely that you’ll overspend to the point where payments are skipped or missed. Create the budget that you can stick to with a payment schedule that you can meet. When you stay in charge of your finances, you decide when it’s time to make a new purchase, whether it be for a home, education, a new vehicle, or another personal expense.

If you know how much money is coming in versus going out each month, it becomes less likely that you’ll overspend to the point where payments are skipped or missed. Create the budget that you can stick to with a payment schedule that you can meet. When you stay in charge of your finances, you decide when it’s time to make a new purchase, whether it be for a home, education, a new vehicle, or another personal expense. Flitter Milz is a nationally recognized consumer protection law firm that represents victims with consumer credit problems, such as credit reporting accuracy and privacy issues, abusive debt collection tactics, wrongful vehicle repossession, which stem from over-spending. If you have errors on your credit reports, have received contact from debt collectors, or your auto lender has repossessed your vehicle,

Flitter Milz is a nationally recognized consumer protection law firm that represents victims with consumer credit problems, such as credit reporting accuracy and privacy issues, abusive debt collection tactics, wrongful vehicle repossession, which stem from over-spending. If you have errors on your credit reports, have received contact from debt collectors, or your auto lender has repossessed your vehicle,