Solar energy can provide benefits to many homeowners — from the financial reward of savings on energy bills, to the ecological benefits of “going green”. While some folks may see a home with a solar power system as an added benefit, others may find it undesirable.

Regardless, the consideration of solar power and panels for the home requires research. Homeowners must explore the variety of products, evaluate the best system for the needs of the household, investigate cost savings, compare finance and/or lease terms, and finally, determine whether adding a solar system is right for their budget.

Is solar power is right for you?

Before contacting a solar sales company, the homeowner should take time to evaluate whether adding solar panels to the home would provide enough financial benefit, plus meet the energy needs of the household. Factors for consideration are: house size, roof — condition and dimensions, climate zone, community regulations, local electricity rates and government incentives. As well, the homeowner may contemplate the following:

Before contacting a solar sales company, the homeowner should take time to evaluate whether adding solar panels to the home would provide enough financial benefit, plus meet the energy needs of the household. Factors for consideration are: house size, roof — condition and dimensions, climate zone, community regulations, local electricity rates and government incentives. As well, the homeowner may contemplate the following:

Current energy usage?

Am I using my energy wisely? Will solar panels reduce my monthly energy bill?

Review your energy bill for usage.  Determine ways that may reduce the current expense such as, changing light bulbs; installing dimmers; fixing a leaking faucet; repairing ductwork. Understand your cost of energy and how much you might save by changing to solar.

Determine ways that may reduce the current expense such as, changing light bulbs; installing dimmers; fixing a leaking faucet; repairing ductwork. Understand your cost of energy and how much you might save by changing to solar.

Sunlight Exposure?

Does my roof get enough sunlight throughout the year?

Evaluate the sun’s path during daylight hours. How many hours of the day does the roof get sunlight? Calculate the number of hours that your roof is shaded. Does the sun/shade ratio change from season-to-season? Would solar panels provide the same benefit throughout the year?

Evaluate the sun’s path during daylight hours. How many hours of the day does the roof get sunlight? Calculate the number of hours that your roof is shaded. Does the sun/shade ratio change from season-to-season? Would solar panels provide the same benefit throughout the year?

Roof Condition?

Does the roof need repair before adding solar panels?

Does the roof and/or shingles require repair or replacement before installation of panels? Will the roof handle the weight of solar panels? Shall I contact an independent roofer to evaluate the roof’s condition?

Does the roof and/or shingles require repair or replacement before installation of panels? Will the roof handle the weight of solar panels? Shall I contact an independent roofer to evaluate the roof’s condition?

Tree Removal?

Do I need to remove trees to create more sunlight for my home?

Review landscaping around the property for sun exposure to the roof. Will panels get enough sunlight to perform at maximum efficiency? Consult with an arborist to estimate tree growth over a 25 year period and the impact of sunlight over the seasons. Will trees require removal or transplant?

Review landscaping around the property for sun exposure to the roof. Will panels get enough sunlight to perform at maximum efficiency? Consult with an arborist to estimate tree growth over a 25 year period and the impact of sunlight over the seasons. Will trees require removal or transplant?

Is solar power free?

Often, prospective customers for solar systems are told the panels will be free. But, we must know, there is no such thing as a free lunch…and in this case, no such thing as free solar panels. Customers will pay for the electricity that is produced by the panels, usually under a solar lease or power purchase agreement. What is the difference?

Solar Panel Lease

A solar lease is a contractual agreement between the homeowner and the solar energy company for installation of solar panels on the roof of the home. Usually, there is no down payment and the solar company is responsible for maintenance. The homeowner makes monthly payments to the solar leasing company at a fixed monthly amount or sells the electricity generated from the panels at a set price per Kilowatt-hour. The solar company is also entitled to all the rebates, tax breaks and incentives for solar power. Solar leases typically last 20 – 25 years.

Power Purchase Agreement (PPA)

A Power Purchase Agreement is an arrangement in which the solar company plans for the design, permitting, financing and installation of a solar energy system on a customer’s property. The homeowner does not own the hardware — the panels or inverter. The solar company sells the power generated to the homeowner at a fixed rate that is typically lower than the local utility’s retail rate. This lower electricity price serves to offset the customer’s purchase of electricity from the grid while the solar company receives the income from the sale of electricity as well as any tax credits and other incentives generated from the system.

PPAs typically range from 10 to 25 years and the solar company usually places a lien on the property. The solar company remains responsible for the operation and maintenance of the system for the duration of the agreement. At the end of the PPA contract term, a customer may be able to extend the PPA, have the solar system removed or choose to buy the solar energy system from them.

Buying, Selling or Refinancing a Home with Solar Panels

Before entering an agreement for a solar power system, whether as an initial purchase, refinancing an existing contract, or purchasing a home with an existing system, you, the consumer, must obtain a copy of the solar panel contract. Take time to review the terms of the agreement. If you need clarification, consult with a real estate agent or real estate attorney for explanation of your legal and financial obligation. Determine whether this agreement is right for you by evaluating:

Before entering an agreement for a solar power system, whether as an initial purchase, refinancing an existing contract, or purchasing a home with an existing system, you, the consumer, must obtain a copy of the solar panel contract. Take time to review the terms of the agreement. If you need clarification, consult with a real estate agent or real estate attorney for explanation of your legal and financial obligation. Determine whether this agreement is right for you by evaluating:

-Monthly cost for panels

-Monthly cost for power

-Full term of lease or finance agreement.

Common questions:

-Ask whether you are able to assume the solar contract from the seller?

-Find out if the panels were purchased or leased.

-Inquire whether there is a lien on the property for the panels?

-Must the lien be satisfied before the sale?

-Does the solar panel contract allow for transfer to a new home buyer?

-Does the warranty transfer to the new home buyer?

Seek Legal Help from a Qualified Consumer Law Firm

Flitter Milz is a nationally recognized consumer protection law firm that evaluates solar panel sales matters for potential violation of the consumer laws involving fraud, such as forged contracts, identity theft and credit reporting privacy violations. Contact Us

Flitter Milz is a nationally recognized consumer protection law firm that evaluates solar panel sales matters for potential violation of the consumer laws involving fraud, such as forged contracts, identity theft and credit reporting privacy violations. Contact Us

Pictured: Cary Flitter (center), Andy Milz (left), Jody López-Jacobs (right).

While most repossessions are initiated by the lender, sometimes it’s the borrower that decides to voluntarily surrender his or her vehicle. Whether or not, after a repossession it’s important for the borrower to understand his or her financial responsibility to satisfy the loan once the lender has taken possession of the vehicle.

While most repossessions are initiated by the lender, sometimes it’s the borrower that decides to voluntarily surrender his or her vehicle. Whether or not, after a repossession it’s important for the borrower to understand his or her financial responsibility to satisfy the loan once the lender has taken possession of the vehicle. can’t meet the terms agreed upon in their auto loan agreement.

can’t meet the terms agreed upon in their auto loan agreement. First, after taking back the vehicle, the lender will send a repossession notice, or

First, after taking back the vehicle, the lender will send a repossession notice, or

The hard facts about Repossession.

The hard facts about Repossession. When the borrower

When the borrower  Whether or not the borrower defaulted on the terms of the auto loan, State and Federal laws govern how lenders and repo agents are to

Whether or not the borrower defaulted on the terms of the auto loan, State and Federal laws govern how lenders and repo agents are to  Send Effective Disputes

Send Effective Disputes

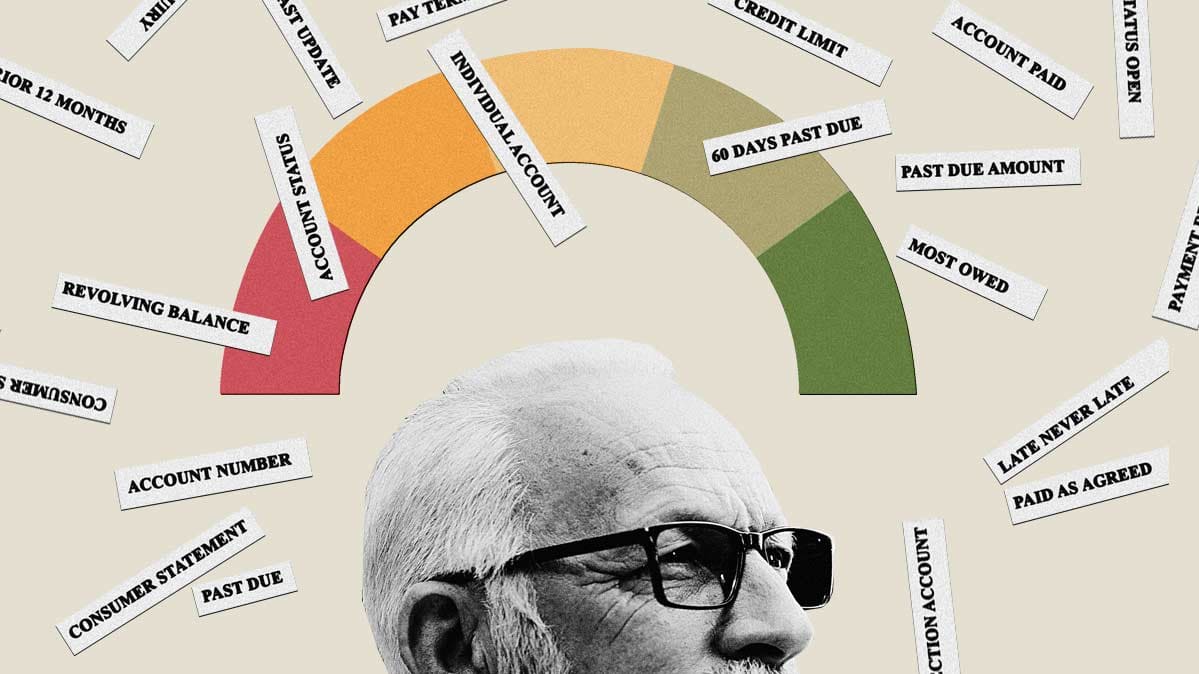

Attorney Andy Milz, cautions consumers that COVID-19-related payment deferrals aren’t the only problem contributing to credit reporting errors and drops in credit scores since the pandemic. He states, in this recent Consumer Reports article, that other common credit reporting errors, such as accounts or loans that have been paid off but still appear as unpaid, individual loans reported multiple times, or debt that’s listed as in collections but has been paid off, can pose hurdles, too, if you need a loan or line of credit.

Attorney Andy Milz, cautions consumers that COVID-19-related payment deferrals aren’t the only problem contributing to credit reporting errors and drops in credit scores since the pandemic. He states, in this recent Consumer Reports article, that other common credit reporting errors, such as accounts or loans that have been paid off but still appear as unpaid, individual loans reported multiple times, or debt that’s listed as in collections but has been paid off, can pose hurdles, too, if you need a loan or line of credit. Consumers are entitled to

Consumers are entitled to  If you notice errors on your credit reports, you must

If you notice errors on your credit reports, you must  Flitter Milz is a nationally recognized consumer protection law firm that represents consumers in matters where the credit bureaus or credit furnishers have continued to report errors on credit reports.

Flitter Milz is a nationally recognized consumer protection law firm that represents consumers in matters where the credit bureaus or credit furnishers have continued to report errors on credit reports.

An individual or business may request access to a consumer’s credit file, but they must obtain written permission from the consumer. Often, during the process of applying for credit, interviewing with a prospective employer or landlord, or applying for utilities, there may be a request to access the consumer’s credit file. Many times the credit application will serve as written permission. Other times, a specific document will be presented to the consumer for his or her signature.

An individual or business may request access to a consumer’s credit file, but they must obtain written permission from the consumer. Often, during the process of applying for credit, interviewing with a prospective employer or landlord, or applying for utilities, there may be a request to access the consumer’s credit file. Many times the credit application will serve as written permission. Other times, a specific document will be presented to the consumer for his or her signature. Consumers must

Consumers must

Being asked to co-sign a loan for a family member or close friend is a larger responsibility than most people realize. When you co-sign a loan, such as an auto loan, you and your credit are on the hook if that relative or friend decides to stop making payments on the loan. In other words, by co-signing, you are a co-borrower and must accept responsibility of terms stated in the loan agreement.

Being asked to co-sign a loan for a family member or close friend is a larger responsibility than most people realize. When you co-sign a loan, such as an auto loan, you and your credit are on the hook if that relative or friend decides to stop making payments on the loan. In other words, by co-signing, you are a co-borrower and must accept responsibility of terms stated in the loan agreement. Once the vehicle is sold, the lender may assign collection of the deficient balance to a debt collector or law firm collector. If the loan balance is not paid, the lender could choose to

Once the vehicle is sold, the lender may assign collection of the deficient balance to a debt collector or law firm collector. If the loan balance is not paid, the lender could choose to  Co-signing a loan should not be taken casually. The co-signer must consider whether or not credit may be needed for him or herself. If a co-signer has too much

Co-signing a loan should not be taken casually. The co-signer must consider whether or not credit may be needed for him or herself. If a co-signer has too much  individual the money for the purchase. In other words, you lend the individual the money and they pay you back in installments over time, or whatever agreement the two of you come up with.

individual the money for the purchase. In other words, you lend the individual the money and they pay you back in installments over time, or whatever agreement the two of you come up with. There may be a knock on your door by a friendly solar panel sales representative. You may be informed of the benefits of solar power and that by choosing to get panels for your home they would be ‘free’.

There may be a knock on your door by a friendly solar panel sales representative. You may be informed of the benefits of solar power and that by choosing to get panels for your home they would be ‘free’. A solar company sales representative may inform you that by signing up for solar power, you won’t have to pay for the panels themselves — they will be given to you for free.

A solar company sales representative may inform you that by signing up for solar power, you won’t have to pay for the panels themselves — they will be given to you for free. Because both of these types of arrangements – a lease and a PPA – involve paying for electricity-generating equipment over a lengthy contract period, those ‘free’ panels that you were promised may be anything but. Once installed on your home’s roof, you will still end up paying toward an entire system that is leased or rented, for a number of years. In the end, the savings you may reap from the solar generated electricity itself may not be enough to make up for those ‘free’ panels.

Because both of these types of arrangements – a lease and a PPA – involve paying for electricity-generating equipment over a lengthy contract period, those ‘free’ panels that you were promised may be anything but. Once installed on your home’s roof, you will still end up paying toward an entire system that is leased or rented, for a number of years. In the end, the savings you may reap from the solar generated electricity itself may not be enough to make up for those ‘free’ panels. Many door-to-door solar sales representatives often ask the consumer to make quick, on-the-spot decisions about obtaining solar power for the home. It is not unusual for the homeowner to feel pressured and the need to act immediately.

Many door-to-door solar sales representatives often ask the consumer to make quick, on-the-spot decisions about obtaining solar power for the home. It is not unusual for the homeowner to feel pressured and the need to act immediately. Flitter Milz is a nationally recognized consumer protection law firm experienced in evaluating fraudulent sales tactics, such as forgery, identity theft and unauthorized credit pulls by solar panel salesmen. If you feel as though you may have been

Flitter Milz is a nationally recognized consumer protection law firm experienced in evaluating fraudulent sales tactics, such as forgery, identity theft and unauthorized credit pulls by solar panel salesmen. If you feel as though you may have been

J

J

2. Obtain Current Credit Reports. Transunion, Experian and Equifax are the three main credit reporting agencies. Consumers are entitled to receive one free credit report from each bureau every year. Sometimes, consumers choose to enroll in a credit monitoring service which enables review of credit reports on a regular basis throughout the year.

2. Obtain Current Credit Reports. Transunion, Experian and Equifax are the three main credit reporting agencies. Consumers are entitled to receive one free credit report from each bureau every year. Sometimes, consumers choose to enroll in a credit monitoring service which enables review of credit reports on a regular basis throughout the year. 4. If Inaccurate…Dispute! After obtaining your credit report, if there are errors, you should

4. If Inaccurate…Dispute! After obtaining your credit report, if there are errors, you should  One Dispute Letter Per Error. If you find multiple errors on a credit report, dispute them individually with the bureau. Enclose a copy of the credit report with the error highlighted and your supporting documents. The credit bureaus then have 30 days to respond to your dispute letter.

One Dispute Letter Per Error. If you find multiple errors on a credit report, dispute them individually with the bureau. Enclose a copy of the credit report with the error highlighted and your supporting documents. The credit bureaus then have 30 days to respond to your dispute letter. The Fair Credit Reporting Act

The Fair Credit Reporting Act  Flitter Milz, P.C. represents people in consumer credit matters related to credit reporting accuracy and privacy, abusive debt collection contact and vehicle repossessions which stem from a pending divorce or separation.

Flitter Milz, P.C. represents people in consumer credit matters related to credit reporting accuracy and privacy, abusive debt collection contact and vehicle repossessions which stem from a pending divorce or separation.