As a college student, your credit is probably one of the last things on your mind. It can be a challenge to balance your classes and coursework while responsibly managing your finances, especially if this is the first time you have had to manage and budget your money.

Many students don’t realize that they start to build their credit right away once they take out student loans, or have expenses like utilities and rent.

If you continue to regularly monitor your credit report, pay bills on time, and keep your credit utilization low, your overall credit will remain in great standing. Good credit after college will make it easier for you to purchase a car, rent without a cosigner, and may even help you secure a job.

Tips for Building Credit

As a young person, you may not have a very extensive credit history. Unless a parent listed you as an authorized user on a credit card, your history is probably minimal. Sparse information may make it more difficult for you to secure new lines of credit or loans without a cosigner because lenders can’t be certain of your likeliness to make timely payments.

If you have student loans, these accounts will appear on your credit report and reflect positively as long as you make payments on time and in full. If you’re struggling with payments, look into income-based repayment options to avoid going into default.

You may also want to consider opening a credit card if you don’t already have one. Different types of accounts add diversity to your credit portfolio and will reflect positively on your score. Shop around for a card with little to no annual fees. Older accounts are more beneficial to your history, so the account will continue to positively affect your credit over time as long as you make payments in full and on time.

Tips for Monitoring Credit

Request your Credit Report

Every twelve months you are entitled to obtain a free credit report from each Transunion, Experian and Equifax. It’s important to regularly monitor your reports, even as a student, because there could be errors that negatively affect it. Write for a copy of your report and have it mailed to you.

Dispute Errors on your Credit Report

Although the credit bureaus have similar listings, the information that appears on one report may differ from another. Be sure to obtain copies of all three reports and review them carefully. If you find an error on your credit report, be sure to send a written dispute to those credit bureaus. You may also want to dispute the error with the creditor. Be sure to include any documents and relevant information that supports your claim.

Keep Your Credit Utilization Low

Your credit utilization also plays an important role in your overall credit health. If you regularly use more than 30% of your available credit, this may have a negative impact on your score. For example, if you have a credit card with a $1000 credit limit, you should avoid spending more than $300. This shows that you’re not only using a small amount of the credit that’s being loaned to you, but that you are using the credit responsibly and paying the amount borrowed.

Seek Legal Help

Flitter Milz is a consumer protection law firm that represents victims with problems involving credit reporting issues, debt collection harassment and vehicle repossessions. Contact Us for a free consultation to discuss your consumer credit issues. If your rights have been violated, our firm will sue the credit bureau, debt collector or lender at no cost to you.

Before applying for any new line of credit, it’s good practice to

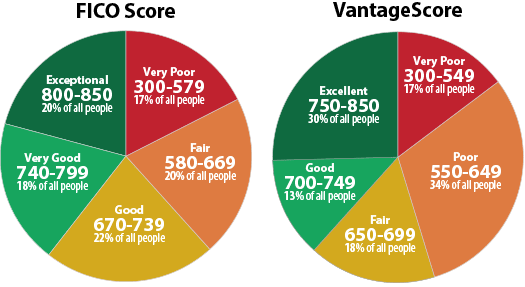

Before applying for any new line of credit, it’s good practice to  However, credit scores that fall in the non-prime (620-679) and subprime (550-619) ranges may not necessarily indicate that you aren’t eligible for a reasonable interest rate. Lenders often use different tiers according to their own business needs to assess creditworthiness.

However, credit scores that fall in the non-prime (620-679) and subprime (550-619) ranges may not necessarily indicate that you aren’t eligible for a reasonable interest rate. Lenders often use different tiers according to their own business needs to assess creditworthiness. Flitter Milz is a consumer protection law firm that pursues matters against lenders, debt collectors and the credit bureaus. If a lender wrongfully repossesses a vehicle, a debt collector is abusive or the credit bureaus report information inaccurately, the consumer may have a lawsuit to pursue. For a no cost legal evaluation,

Flitter Milz is a consumer protection law firm that pursues matters against lenders, debt collectors and the credit bureaus. If a lender wrongfully repossesses a vehicle, a debt collector is abusive or the credit bureaus report information inaccurately, the consumer may have a lawsuit to pursue. For a no cost legal evaluation,

A

A  When you need to secure a loan for the purchase of your new vehicle,

When you need to secure a loan for the purchase of your new vehicle,

Protection from Repossession

Protection from Repossession After a vehicle has been repossessed, the lender is required to send proper notices to the borrower. Shortly after the repossession, the lender will send a letter called a Notice of Intent to Sell Property, which confirms the repossession occurred and details terms for to retrieve the vehicle. If the borrower is not able to meet the terms, the lender may choose to sell the vehicle at an auction or private sale. Once the sale has taken place, the lender will send a second letter called a Deficiency Notice, which informs the borrower of the sale price of the vehicle and any remaining balance due. If the borrower is not notified properly, there may be grounds to file a lawsuit against the lender.

After a vehicle has been repossessed, the lender is required to send proper notices to the borrower. Shortly after the repossession, the lender will send a letter called a Notice of Intent to Sell Property, which confirms the repossession occurred and details terms for to retrieve the vehicle. If the borrower is not able to meet the terms, the lender may choose to sell the vehicle at an auction or private sale. Once the sale has taken place, the lender will send a second letter called a Deficiency Notice, which informs the borrower of the sale price of the vehicle and any remaining balance due. If the borrower is not notified properly, there may be grounds to file a lawsuit against the lender. If you’re

If you’re  First and foremost, if there’s a chance that your vehicle will be repossessed, you should take the following actions in preparation:

First and foremost, if there’s a chance that your vehicle will be repossessed, you should take the following actions in preparation: Many consumers who anticipate a repossession wonder if the consequences will be less negative if they voluntarily surrender the vehicle to the lender. The only significant difference between the two is the way they appear on your credit report; a voluntary surrender will be listed as such, but the negative effect will be about the same as a repossession. It’s possible, however, that the lender will be more willing to enter a loan agreement with you in the future if you voluntarily surrender the vehicle.

Many consumers who anticipate a repossession wonder if the consequences will be less negative if they voluntarily surrender the vehicle to the lender. The only significant difference between the two is the way they appear on your credit report; a voluntary surrender will be listed as such, but the negative effect will be about the same as a repossession. It’s possible, however, that the lender will be more willing to enter a loan agreement with you in the future if you voluntarily surrender the vehicle. If you are having difficulty making payments, contact your lender as soon as possible. You may be able to avoid repossession by

If you are having difficulty making payments, contact your lender as soon as possible. You may be able to avoid repossession by  Whether you have fallen behind on your car payments or not, there are legal protections for borrowers from lenders and repo agents that wrongfully repossess vehicles.

Whether you have fallen behind on your car payments or not, there are legal protections for borrowers from lenders and repo agents that wrongfully repossess vehicles.