Purchasing a new vehicle is a major decision, especially when you need to secure a loan in order to do so. Not only are you shopping for a car, you’re also shopping for the best interest rate and loan agreement terms. This process can be even more difficult if you have poor credit.

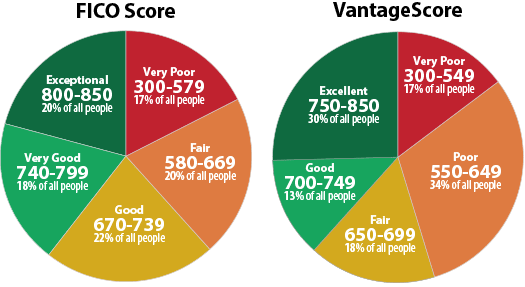

Check your credit before the purchase

A negative credit history can make it more difficult to find an agreement with reasonable interest rates and can also make it more challenging to get your application approved. It’s important to prepare and research ahead of time before you make a decision to ensure that you choose the best option for your situation. You may run the risk of a vehicle repossession when the loan agreement terms present challenges to your finances.

A negative credit history can make it more difficult to find an agreement with reasonable interest rates and can also make it more challenging to get your application approved. It’s important to prepare and research ahead of time before you make a decision to ensure that you choose the best option for your situation. You may run the risk of a vehicle repossession when the loan agreement terms present challenges to your finances.

The vehicle is collateral to the lender

The vehicle is considered collateral in a loan agreement. As the borrower pledges repayment of the loan, collateral is a form of security for the lender. If a borrower fails to make payments under the loan agreement, the lender has the right to repossess the vehicle. A repossession will further harm your credit and negatively impact your history for up to seven and a half years.

Shop for the loan that is right for you.

When you need to secure a loan for the purchase of your new vehicle, take steps to make sure you get the loan that is right for you. If you enter a loan agreement with unfavorable terms, you may not be able to make loan payments in full and on time. When the terms of the loan have been broken, the lender may take steps to repossess your vehicle.

When you need to secure a loan for the purchase of your new vehicle, take steps to make sure you get the loan that is right for you. If you enter a loan agreement with unfavorable terms, you may not be able to make loan payments in full and on time. When the terms of the loan have been broken, the lender may take steps to repossess your vehicle.

Seek Legal Advice

Flitter Milz is knowledgeable about the laws governing repossession of cars, trucks, motorcycles, boats and RVs. If your vehicle has been repossessed, Contact Us. We will review the details of your case at no cost, and evaluate whether your consumer rights were violated.

Flitter Milz is knowledgeable about the laws governing repossession of cars, trucks, motorcycles, boats and RVs. If your vehicle has been repossessed, Contact Us. We will review the details of your case at no cost, and evaluate whether your consumer rights were violated.

Repossessing a Vehicle

Repossessing a Vehicle

The lender will send a written

The lender will send a written  If your car, truck, motorcycle, boat, or RV has been repossessed, a qualified consumer protection attorney can evaluate whether your rights have been violated. It will be important for you to provide a copy of your signed

If your car, truck, motorcycle, boat, or RV has been repossessed, a qualified consumer protection attorney can evaluate whether your rights have been violated. It will be important for you to provide a copy of your signed  Whether you fell behind on payments or not, borrowers have legal rights when the lender or repo agent has wrongfully repossessed the vehicle. Flitter Milz is a nationally recognized consumer protection law firm that represents consumers who have had a vehicle wrongfully repossessed.

Whether you fell behind on payments or not, borrowers have legal rights when the lender or repo agent has wrongfully repossessed the vehicle. Flitter Milz is a nationally recognized consumer protection law firm that represents consumers who have had a vehicle wrongfully repossessed.  Protection from Repossession

Protection from Repossession After a vehicle has been repossessed, the lender is required to send proper notices to the borrower. Shortly after the repossession, the lender will send a letter called a Notice of Intent to Sell Property, which confirms the repossession occurred and details terms for to retrieve the vehicle. If the borrower is not able to meet the terms, the lender may choose to sell the vehicle at an auction or private sale. Once the sale has taken place, the lender will send a second letter called a Deficiency Notice, which informs the borrower of the sale price of the vehicle and any remaining balance due. If the borrower is not notified properly, there may be grounds to file a lawsuit against the lender.

After a vehicle has been repossessed, the lender is required to send proper notices to the borrower. Shortly after the repossession, the lender will send a letter called a Notice of Intent to Sell Property, which confirms the repossession occurred and details terms for to retrieve the vehicle. If the borrower is not able to meet the terms, the lender may choose to sell the vehicle at an auction or private sale. Once the sale has taken place, the lender will send a second letter called a Deficiency Notice, which informs the borrower of the sale price of the vehicle and any remaining balance due. If the borrower is not notified properly, there may be grounds to file a lawsuit against the lender.

Flitter Milz is a nationally recognized consumer protection law firm that represents victims of improper vehicle repossessions. If you think your consumer rights may have been violated by the lender or repo agent,

Flitter Milz is a nationally recognized consumer protection law firm that represents victims of improper vehicle repossessions. If you think your consumer rights may have been violated by the lender or repo agent,