Be sure to request your credit report and verify that your credit history is up to date and accurate before seeking a new job. Prospective employers often run credit checks on potential employees prior to making hiring decisions, and negative listings could hurt your chances for employment or a promotion. The Fair Credit Reporting Act (FCRA) is the law that requires employers to obtain a prospective hire’s consent prior to pulling a credit file.

Employers Must Obtain Permission

Employers must obtain your written permission before they can access your credit file. During the application process, the employer should provide you with background check disclosure and authorization forms that require your signature.

Easy to Understand Forms

The Federal Trade Commission (FTC) states that these authorization forms should be free of “complicated legal jargon” or “extra acknowledgement or waivers.” You should never feel confused or misled when it comes to authorization forms that an employer or prospective employer provides in order to get your consent to view your credit.

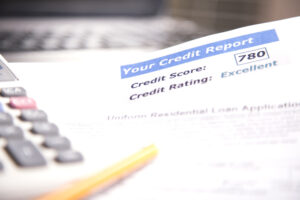

Your Right to View the Report

You also have the right to see the report that the employer used as a means to determine your employment. You should inform the prospective employer that you want to have a copy whether you are hired or not.

Seek Legal Advice

Flitter Milz is a nationally recognized consumer protection law firm that represents victims of inaccurate credit reporting. Contact us for a free evaluation of your reports.

If you’re

If you’re  First and foremost, if there’s a chance that your vehicle will be repossessed, you should take the following actions in preparation:

First and foremost, if there’s a chance that your vehicle will be repossessed, you should take the following actions in preparation: Many consumers who anticipate a repossession wonder if the consequences will be less negative if they voluntarily surrender the vehicle to the lender. The only significant difference between the two is the way they appear on your credit report; a voluntary surrender will be listed as such, but the negative effect will be about the same as a repossession. It’s possible, however, that the lender will be more willing to enter a loan agreement with you in the future if you voluntarily surrender the vehicle.

Many consumers who anticipate a repossession wonder if the consequences will be less negative if they voluntarily surrender the vehicle to the lender. The only significant difference between the two is the way they appear on your credit report; a voluntary surrender will be listed as such, but the negative effect will be about the same as a repossession. It’s possible, however, that the lender will be more willing to enter a loan agreement with you in the future if you voluntarily surrender the vehicle. If you are having difficulty making payments, contact your lender as soon as possible. You may be able to avoid repossession by

If you are having difficulty making payments, contact your lender as soon as possible. You may be able to avoid repossession by  Whether you have fallen behind on your car payments or not, there are legal protections for borrowers from lenders and repo agents that wrongfully repossess vehicles.

Whether you have fallen behind on your car payments or not, there are legal protections for borrowers from lenders and repo agents that wrongfully repossess vehicles.  Before agreeing to a loan with one of these dealerships, be sure to shop around and see if there is a bank, credit union or other lender who is willing to loan to you. An auto loan with high interest rates, like those that typically come from buy here – pay here dealerships, may not be worth it; the cost of the loan could outweigh the benefit of purchasing the vehicle. Learn more about

Before agreeing to a loan with one of these dealerships, be sure to shop around and see if there is a bank, credit union or other lender who is willing to loan to you. An auto loan with high interest rates, like those that typically come from buy here – pay here dealerships, may not be worth it; the cost of the loan could outweigh the benefit of purchasing the vehicle. Learn more about  Before visiting the car dealership, it’s important to

Before visiting the car dealership, it’s important to  Flitter Milz is a consumer protection law firm that represents people that defaulted on auto loan payments and had a vehicle repossessed.

Flitter Milz is a consumer protection law firm that represents people that defaulted on auto loan payments and had a vehicle repossessed.  When you’re in the market to purchase a new vehicle and need to

When you’re in the market to purchase a new vehicle and need to  There are a number of factors that will affect your auto loan agreement, but the most important is your credit history. Before you start shopping for interest rates, check your

There are a number of factors that will affect your auto loan agreement, but the most important is your credit history. Before you start shopping for interest rates, check your  Flitter Milz is a consumer protection law firm that represents borrowers that have defaulted on their auto loan. Whether payments have been missed or not, the lender must follow the law.

Flitter Milz is a consumer protection law firm that represents borrowers that have defaulted on their auto loan. Whether payments have been missed or not, the lender must follow the law.