The hard facts about Repossession.

The hard facts about Repossession.

We all understand that when you borrow money, you need to pay it back. And if you take out an auto loan, whether it’s with a bank, credit union or other financial institution, if payments are late or missed, the lender has the right to repossess the vehicle.

Signing a loan agreement means that you agree to the terms to repay the money borrowed, plus any interest and fees, within a scheduled period of time. Opting to finance a vehicle is an important decision and carries significant responsibility and financial discipline.

Short Term v. Long Term Effects of Repossession

When the borrower defaults on an auto loan there are serious consequences. Immediately, daily life becomes upset without use of the car. Getting to work or handling routine daily chores, such as food shopping, taking children to school, or attending doctor’s appointments, may present difficulties for the household.

When the borrower defaults on an auto loan there are serious consequences. Immediately, daily life becomes upset without use of the car. Getting to work or handling routine daily chores, such as food shopping, taking children to school, or attending doctor’s appointments, may present difficulties for the household.

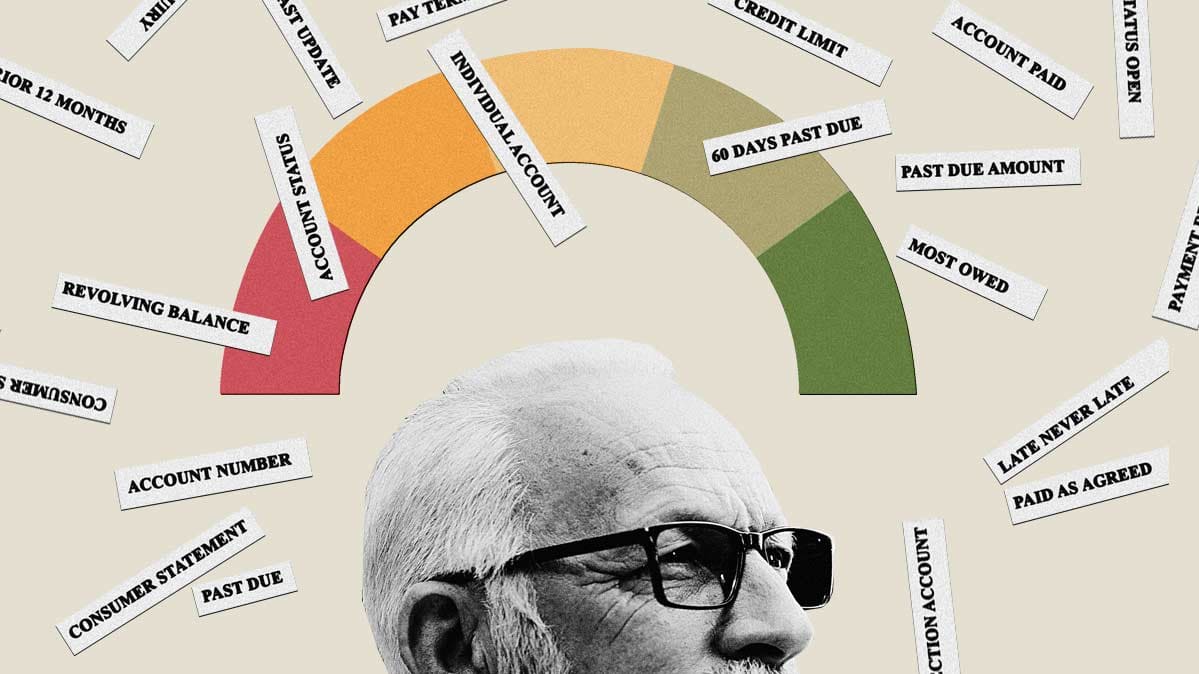

But more important is the long-term consequence. Repossessions can remain on credit reports for seven-and-one-half years, beginning from the date that the account first became delinquent. And, as long as the repossession stays on your report, it can seriously damage credit and impact the calculation of credit scores. Also, negative listings on credit reports may make it more difficult to secure new loans, and existing creditors could alter credit terms by lowering credit limits or increasing interest rates.

Factors that can Damage Credit

- Late payments – every month a payment is missed a negative mark appears on the account’s payment history.

- Defaults – Loan defaults carry negative weight. i.e. charge-off or repossession.

- Collections – Collection accounts appear as negative listings on credit reports.

- Court Judgments – Unsuccessful collection attempts, lead to lawsuits against the borrower to obtain a judgment.

Factors Contributing to the Calculation of a Credit Score

- Payment History – Timely payments made to an account

- Credit Utilization – The ratio of available to used credit

- Age of Credit – The length of time an account has been open

- Types of Accounts – A consumer’s credit mix: mortgage, credit cards, loans, etc.

- Application history – The number of credit applications submitted within a specific period

Legal Protections from a Wrongful Repossessions

Whether or not the borrower defaulted on the terms of the auto loan, State and Federal laws govern how lenders and repo agents are to handle repossessions properly– at the scene and afterwards. When the borrower’s consumer rights are violated, a case could be pursued against the lender, repo agent or both. Repo agents may not threaten the borrower or use physical force. In the course of repossession, the borrower’s vehicle or property is not to be damaged. If police are called to the scene, their job is to keep the peace, not assist with the repossession. If personal items have been left in the repossessed vehicle, the repo agent must permit the borrower to retrieve those items.

Whether or not the borrower defaulted on the terms of the auto loan, State and Federal laws govern how lenders and repo agents are to handle repossessions properly– at the scene and afterwards. When the borrower’s consumer rights are violated, a case could be pursued against the lender, repo agent or both. Repo agents may not threaten the borrower or use physical force. In the course of repossession, the borrower’s vehicle or property is not to be damaged. If police are called to the scene, their job is to keep the peace, not assist with the repossession. If personal items have been left in the repossessed vehicle, the repo agent must permit the borrower to retrieve those items.

AFTER the Repossession

Following the repossession the lender has responsibilities to the borrower. They must provide notices that inform the borrower with steps to retrieve the vehicle and their personal property. Once the vehicle is sold, the lender must inform the borrower of the selling price and present a calculation of any remaining balance owed to satisfy the loan.

Manage Auto Loan Payments and Credit Reporting

Monitor Credit Reports for Errors

Over the course of the auto loan, borrowers should monitor their Transunion, Experian and Equifax credit reports for accurate reporting. If incorrect information is listed, such as a late payment history, a dispute letter should be sent to the lender and the credit bureau to request correction on the report.

Send Effective Disputes

Send Effective Disputes

Disputes letters must include documents that show the error, such as cancelled checks, account statements, correspondence with the lender, etc. Also, the dispute must clearly state the requested action, an update, correction or removal of the information.

Keep Accurate Payment Records

As important as it is to make payments in full and on time, we can’t always rely on the lender to keep an accurate record of payments. Sometimes mistakes are made. Incorrect payment amounts could be applied to the borrower’s account, or the payment could be applied to someone else’s account. Borrowers that manage and keep accurate payment records have good documents to support disputes made to the lender and/or credit bureau.

Seek advice from a Qualified Repossession Lawyers

Flitter Milz is a nationally recognized consumer protection law firm that represents consumers in matters of wrongful repossessions and credit reporting accuracy and privacy disputes. When errors remain on credit reports after a dispute, Contact Us for a no cost legal review to determine whether your consumer rights have been violated. Pictured: Cary Flitter (center), Andy Milz (left), Jody López-Jacobs (right).

Flitter Milz is a nationally recognized consumer protection law firm that represents consumers in matters of wrongful repossessions and credit reporting accuracy and privacy disputes. When errors remain on credit reports after a dispute, Contact Us for a no cost legal review to determine whether your consumer rights have been violated. Pictured: Cary Flitter (center), Andy Milz (left), Jody López-Jacobs (right).

Attorney Andy Milz, cautions consumers that COVID-19-related payment deferrals aren’t the only problem contributing to credit reporting errors and drops in credit scores since the pandemic. He states, in this recent Consumer Reports article, that other common credit reporting errors, such as accounts or loans that have been paid off but still appear as unpaid, individual loans reported multiple times, or debt that’s listed as in collections but has been paid off, can pose hurdles, too, if you need a loan or line of credit.

Attorney Andy Milz, cautions consumers that COVID-19-related payment deferrals aren’t the only problem contributing to credit reporting errors and drops in credit scores since the pandemic. He states, in this recent Consumer Reports article, that other common credit reporting errors, such as accounts or loans that have been paid off but still appear as unpaid, individual loans reported multiple times, or debt that’s listed as in collections but has been paid off, can pose hurdles, too, if you need a loan or line of credit. Consumers are entitled to

Consumers are entitled to  If you notice errors on your credit reports, you must

If you notice errors on your credit reports, you must  Flitter Milz is a nationally recognized consumer protection law firm that represents consumers in matters where the credit bureaus or credit furnishers have continued to report errors on credit reports.

Flitter Milz is a nationally recognized consumer protection law firm that represents consumers in matters where the credit bureaus or credit furnishers have continued to report errors on credit reports.

An individual or business may request access to a consumer’s credit file, but they must obtain written permission from the consumer. Often, during the process of applying for credit, interviewing with a prospective employer or landlord, or applying for utilities, there may be a request to access the consumer’s credit file. Many times the credit application will serve as written permission. Other times, a specific document will be presented to the consumer for his or her signature.

An individual or business may request access to a consumer’s credit file, but they must obtain written permission from the consumer. Often, during the process of applying for credit, interviewing with a prospective employer or landlord, or applying for utilities, there may be a request to access the consumer’s credit file. Many times the credit application will serve as written permission. Other times, a specific document will be presented to the consumer for his or her signature. Consumers must

Consumers must

Being asked to co-sign a loan for a family member or close friend is a larger responsibility than most people realize. When you co-sign a loan, such as an auto loan, you and your credit are on the hook if that relative or friend decides to stop making payments on the loan. In other words, by co-signing, you are a co-borrower and must accept responsibility of terms stated in the loan agreement.

Being asked to co-sign a loan for a family member or close friend is a larger responsibility than most people realize. When you co-sign a loan, such as an auto loan, you and your credit are on the hook if that relative or friend decides to stop making payments on the loan. In other words, by co-signing, you are a co-borrower and must accept responsibility of terms stated in the loan agreement. Once the vehicle is sold, the lender may assign collection of the deficient balance to a debt collector or law firm collector. If the loan balance is not paid, the lender could choose to

Once the vehicle is sold, the lender may assign collection of the deficient balance to a debt collector or law firm collector. If the loan balance is not paid, the lender could choose to  Co-signing a loan should not be taken casually. The co-signer must consider whether or not credit may be needed for him or herself. If a co-signer has too much

Co-signing a loan should not be taken casually. The co-signer must consider whether or not credit may be needed for him or herself. If a co-signer has too much  individual the money for the purchase. In other words, you lend the individual the money and they pay you back in installments over time, or whatever agreement the two of you come up with.

individual the money for the purchase. In other words, you lend the individual the money and they pay you back in installments over time, or whatever agreement the two of you come up with. There may be a knock on your door by a friendly solar panel sales representative. You may be informed of the benefits of solar power and that by choosing to get panels for your home they would be ‘free’.

There may be a knock on your door by a friendly solar panel sales representative. You may be informed of the benefits of solar power and that by choosing to get panels for your home they would be ‘free’. A solar company sales representative may inform you that by signing up for solar power, you won’t have to pay for the panels themselves — they will be given to you for free.

A solar company sales representative may inform you that by signing up for solar power, you won’t have to pay for the panels themselves — they will be given to you for free. Because both of these types of arrangements – a lease and a PPA – involve paying for electricity-generating equipment over a lengthy contract period, those ‘free’ panels that you were promised may be anything but. Once installed on your home’s roof, you will still end up paying toward an entire system that is leased or rented, for a number of years. In the end, the savings you may reap from the solar generated electricity itself may not be enough to make up for those ‘free’ panels.

Because both of these types of arrangements – a lease and a PPA – involve paying for electricity-generating equipment over a lengthy contract period, those ‘free’ panels that you were promised may be anything but. Once installed on your home’s roof, you will still end up paying toward an entire system that is leased or rented, for a number of years. In the end, the savings you may reap from the solar generated electricity itself may not be enough to make up for those ‘free’ panels. Many door-to-door solar sales representatives often ask the consumer to make quick, on-the-spot decisions about obtaining solar power for the home. It is not unusual for the homeowner to feel pressured and the need to act immediately.

Many door-to-door solar sales representatives often ask the consumer to make quick, on-the-spot decisions about obtaining solar power for the home. It is not unusual for the homeowner to feel pressured and the need to act immediately. Flitter Milz is a nationally recognized consumer protection law firm experienced in evaluating fraudulent sales tactics, such as forgery, identity theft and unauthorized credit pulls by solar panel salesmen. If you feel as though you may have been

Flitter Milz is a nationally recognized consumer protection law firm experienced in evaluating fraudulent sales tactics, such as forgery, identity theft and unauthorized credit pulls by solar panel salesmen. If you feel as though you may have been

J

J

2. Obtain Current Credit Reports. Transunion, Experian and Equifax are the three main credit reporting agencies. Consumers are entitled to receive one free credit report from each bureau every year. Sometimes, consumers choose to enroll in a credit monitoring service which enables review of credit reports on a regular basis throughout the year.

2. Obtain Current Credit Reports. Transunion, Experian and Equifax are the three main credit reporting agencies. Consumers are entitled to receive one free credit report from each bureau every year. Sometimes, consumers choose to enroll in a credit monitoring service which enables review of credit reports on a regular basis throughout the year. 4. If Inaccurate…Dispute! After obtaining your credit report, if there are errors, you should

4. If Inaccurate…Dispute! After obtaining your credit report, if there are errors, you should  One Dispute Letter Per Error. If you find multiple errors on a credit report, dispute them individually with the bureau. Enclose a copy of the credit report with the error highlighted and your supporting documents. The credit bureaus then have 30 days to respond to your dispute letter.

One Dispute Letter Per Error. If you find multiple errors on a credit report, dispute them individually with the bureau. Enclose a copy of the credit report with the error highlighted and your supporting documents. The credit bureaus then have 30 days to respond to your dispute letter. The Fair Credit Reporting Act

The Fair Credit Reporting Act  Flitter Milz, P.C. represents people in consumer credit matters related to credit reporting accuracy and privacy, abusive debt collection contact and vehicle repossessions which stem from a pending divorce or separation.

Flitter Milz, P.C. represents people in consumer credit matters related to credit reporting accuracy and privacy, abusive debt collection contact and vehicle repossessions which stem from a pending divorce or separation.

Crafting a household budget is not only necessary to help evaluate spending patterns and measure income versus expenditures, but it also helps to ensure a secure financial future.

Crafting a household budget is not only necessary to help evaluate spending patterns and measure income versus expenditures, but it also helps to ensure a secure financial future. If you know how much money is coming in versus going out each month, it becomes less likely that you’ll overspend to the point where payments are skipped or missed. Create the budget that you can stick to with a payment schedule that you can meet. When you stay in charge of your finances, you decide when it’s time to make a new purchase, whether it be for a home, education, a new vehicle, or another personal expense.

If you know how much money is coming in versus going out each month, it becomes less likely that you’ll overspend to the point where payments are skipped or missed. Create the budget that you can stick to with a payment schedule that you can meet. When you stay in charge of your finances, you decide when it’s time to make a new purchase, whether it be for a home, education, a new vehicle, or another personal expense. Flitter Milz is a nationally recognized consumer protection law firm that represents victims with consumer credit problems, such as credit reporting accuracy and privacy issues, abusive debt collection tactics, wrongful vehicle repossession, which stem from over-spending. If you have errors on your credit reports, have received contact from debt collectors, or your auto lender has repossessed your vehicle,

Flitter Milz is a nationally recognized consumer protection law firm that represents victims with consumer credit problems, such as credit reporting accuracy and privacy issues, abusive debt collection tactics, wrongful vehicle repossession, which stem from over-spending. If you have errors on your credit reports, have received contact from debt collectors, or your auto lender has repossessed your vehicle,  The holiday shopping season is, under normal circumstances, a big stressor on the wallet. But this year proposes to be even more difficult than in years past, given that the global COVID-19 pandemic has led to massive job losses and financial hardships for people far and wide. Although the federal

The holiday shopping season is, under normal circumstances, a big stressor on the wallet. But this year proposes to be even more difficult than in years past, given that the global COVID-19 pandemic has led to massive job losses and financial hardships for people far and wide. Although the federal  The danger in over-spending comes when that monthly bill is due, and you are still unable to come up with the cash to pay it off. Not paying

The danger in over-spending comes when that monthly bill is due, and you are still unable to come up with the cash to pay it off. Not paying  Using a credit card makes it easy to over-spend, especially during the holidays. The freedom of making purchases with a credit card today, could make it difficult to pay the bill the following month if purchases get out of hand.

Using a credit card makes it easy to over-spend, especially during the holidays. The freedom of making purchases with a credit card today, could make it difficult to pay the bill the following month if purchases get out of hand. Credit reports

Credit reports Flitter Milz is a nationally recognized consumer protection law firm that represents people with credit reporting accuracy and privacy issues, contact from abusive debt collectors and wrongful repossession. If you are someone who has suffered a hardship during the pandemic and feel as though your consumer rights have been violated by the credit bureaus, a lender or debt collector,

Flitter Milz is a nationally recognized consumer protection law firm that represents people with credit reporting accuracy and privacy issues, contact from abusive debt collectors and wrongful repossession. If you are someone who has suffered a hardship during the pandemic and feel as though your consumer rights have been violated by the credit bureaus, a lender or debt collector,