Most households are looking for ways to reduce costs. Today, utilizing the sun’s power has become an enticing option. Lowering monthly energy bills and contributing to a green environment are common reasons that homeowners opt for solar power. But, choosing to add solar panels to your home is not a casual decision. It requires research, investigation and planning.

Is my home suitable for solar panels?

There are pros and cons to every decision a homeowner makes. Like any other investment, going solar may not make sense for every home. After gathering facts, you need to evaluate:

- Energy usage for the home. How much power must be generated to satisfy the needs of people in the home.

- Condition of the roof. Does the roof need repair or to be replaced? Can my roof handle the weight of panels?

- Location of the home. Am I in the right climate for solar panels?

- Sunlight v. Shade. Does my roof get enough sunlight throughout the day to produce the power needed for my home? Do trees need to be removed from my property for panels to work efficiently?

- Panel configuration. Does my roof have enough space for solar panels?

Shopping Solar Companies & Financing

Similar to purchasing other items for the home, when considering solar panels, homeowners must shop around, get quotes, and investigate solar panel companies to compare one offer from another. There are a wide variety of products on the market with varying levels of efficiency, durability, reliability, output and design. As well, there are a number of solar companies and installers — some are better than others. Check the company’s reputation to see if complaints been filed against them with the Federal Trade Commission, State Attorney General, or Better Business Bureau? Also, searching court dockets for lawsuits that have been filed against solar panel companies or their finance companies may provide insight to issues that other consumer’s have faced involving solar transactions.

Similar to purchasing other items for the home, when considering solar panels, homeowners must shop around, get quotes, and investigate solar panel companies to compare one offer from another. There are a wide variety of products on the market with varying levels of efficiency, durability, reliability, output and design. As well, there are a number of solar companies and installers — some are better than others. Check the company’s reputation to see if complaints been filed against them with the Federal Trade Commission, State Attorney General, or Better Business Bureau? Also, searching court dockets for lawsuits that have been filed against solar panel companies or their finance companies may provide insight to issues that other consumer’s have faced involving solar transactions.

CAUTION #1: Is “Free” really free?

Frequently, we hear about door-to-door solar salesman telling homeowners that the solar panels will be free. After listening to a sales presentation and learning

of the benefits of solar power, the consumer is presented an iPad or tablet to sign, believing their signature gives the salesman permission to evaluate the property for panels. However, the signature, or initials, on an iPad may authorize the solar company, without the consumer’s knowledge, to:

of the benefits of solar power, the consumer is presented an iPad or tablet to sign, believing their signature gives the salesman permission to evaluate the property for panels. However, the signature, or initials, on an iPad may authorize the solar company, without the consumer’s knowledge, to:

-Access the consumer’s credit file.

-Utilize the signature on documents that are Doc-U-Signed

-Enter the consumer in to a contract for solar panels

-Submit applications to finance the panels.

It’s not until panels have been installed on the home and bills begin to arrive that the consumer realizes solar panels are anything but free. Instead, many consumers find that they signed into a decades-long financial commitment which can last for 20 -25 years for the panels. Bills from the local energy provider plus the cost of solar panels make the total cost of energy burdensome. All of a sudden, homeowners finds themselves in thousands of dollars of debt when they thought the panels were for free.

CAUTION #2: Is the solar company reputable?

Before making a commitment to get panels, investigate reviews from other consumers. Obtain quotes from multiple solar companies for comparison. Then decide which company is best for you. For example, do I get panels from SunPower, Momentum Solar or Tesla? Which company offers the product I want to buy? Which company is presenting me with the best system for my home? What types of problems have other consumers faced when getting panels from one company versus another?

CAUTION #3: Why did the solar company access my credit report?

Prospective lenders for solar panels, such as banks, credit unions and financial institutions, seek access to the homeowner’s credit reports to determine whether to extend credit. This can only be done with the consumer’s written permission. When reports are accessed without the consumer’s permission, the consumer’s rights may have been violated. The Fair Credit Reporting Act is a federal law that governs the privacy and accuracy of credit reports. If you do not want your reports accessed, do not sign anything that would grant permission.

CAUTION #4: How do I pay for the solar power system?

If you don’t have cash on hand to pay for the system, you must evaluate whether to lease, enter a power purchase agreement (PPA) or finance the system through a solar loan.

The benefit of entering a solar lease or PPA is that costs are not paid upfront. The solar company owns the system on your roof and monthly payments are made to them for the energy generated by the panels.

Solar loans work like other home improvement loans. The loan is taken out through a finance company with monthly payments made to the lender for the purchase of the system. Just like researching the solar company, homeowners must research the best way to finance the solar power system. There are several companies, such as Goodleap, Mosaic, or Sunlight Financial, that offer loans for solar panels. But ask yourself, which one offers the best terms for me?

Solar loans work like other home improvement loans. The loan is taken out through a finance company with monthly payments made to the lender for the purchase of the system. Just like researching the solar company, homeowners must research the best way to finance the solar power system. There are several companies, such as Goodleap, Mosaic, or Sunlight Financial, that offer loans for solar panels. But ask yourself, which one offers the best terms for me?

For instance: Who is Goodleap?

Formerly known as Loanpal, Goodleap is a finance company that provides loans for solar products like rooftop solar panel systems. Goodleap teams up with door- to-door sales companies who sometimes entice people to sign up for “free” solar panels. Hundreds of consumers have complained about Loanpal/Goodleap’s business practices to the Better Business Bureau. The Better Business Bureau has rated Loanpal an “F.” From customer reviews, Loanpal received only one out of five stars. In fact, some consumers complain that they never saw or signed a contract. When faced with accusations that the solar panel salesperson engaged in fraud — such as signing up a consumer for a loan without their knowledge or consent — Goodleap has attempted to distance itself from the solar panel company.

to-door sales companies who sometimes entice people to sign up for “free” solar panels. Hundreds of consumers have complained about Loanpal/Goodleap’s business practices to the Better Business Bureau. The Better Business Bureau has rated Loanpal an “F.” From customer reviews, Loanpal received only one out of five stars. In fact, some consumers complain that they never saw or signed a contract. When faced with accusations that the solar panel salesperson engaged in fraud — such as signing up a consumer for a loan without their knowledge or consent — Goodleap has attempted to distance itself from the solar panel company.

The salesperson won’t even tell you that Goodleap needs to pull your credit report for a loan. Your “consent” may have been buried in documents that were Doc-U-Signed on the iPad or tablet. And although you may have been promised copies of anything you signed, you never received them. Often, you won’t learn about the existence of any loan papers until the solar panels have been installed on your home. Remember, it is fraudulent and unlawful for anyone to be signed up for a loan without written consent.

How to protect yourself when considering solar

- Get a copy of the contract and read it carefully before signing. There is no rush for you to enter into a deal.

- Never give out personal information – bank account numbers, birth dates, Social Security Number – to a door-to-door salesman you just met.

- Monitor your credit. It is illegal for a solar company to make a hard inquiry on your credit report without a permissible purpose. You must provide written authorization for someone to access your credit file.

- Visit websites for the Federal Trade Commission, Consumer Financial Protection Bureau, State Attorney General, and the Better Business Bureau for insight on solar energy scams.

Seek Legal Help from a Qualified Consumer Law Firm

Flitter Milz is a nationally recognized consumer protection law firm that evaluates solar panel sales matters for potential violation of the consumer laws involving fraud, such as forged contracts, identity theft and credit reporting privacy violations. Contact Us

Flitter Milz is a nationally recognized consumer protection law firm that evaluates solar panel sales matters for potential violation of the consumer laws involving fraud, such as forged contracts, identity theft and credit reporting privacy violations. Contact Us

Pictured: Cary Flitter (center), Andy Milz (left), Jody López-Jacobs (right).

Read more below:

Read more below: There are a variety of reasons why credit files get mixed. With the amount of information handled by creditors and the credit bureaus, mistakes are bound to happen. For example, information from an application may be keyed into a file incorrectly. Digits on a social security number may be transposed, or a name misspelled from an application. Those errors can pass from the original creditor through to the credit bureau. Or, the credit bureau mistakenly may combine credit files of two or more different consumers into one file. Unfortunately, the errors may not be discovered until the consumer reviews his or her report…usually after applying for new credit.

There are a variety of reasons why credit files get mixed. With the amount of information handled by creditors and the credit bureaus, mistakes are bound to happen. For example, information from an application may be keyed into a file incorrectly. Digits on a social security number may be transposed, or a name misspelled from an application. Those errors can pass from the original creditor through to the credit bureau. Or, the credit bureau mistakenly may combine credit files of two or more different consumers into one file. Unfortunately, the errors may not be discovered until the consumer reviews his or her report…usually after applying for new credit. If you believe someone else’s information has been mixed with or merged onto your credit file, a

If you believe someone else’s information has been mixed with or merged onto your credit file, a  The reporting bureau has 30 days to respond to your written dispute. If errors are not corrected, you may need to send a second dispute to that bureau, and possibly provide additional documentation. Or, you may need to write to the underlying creditor, explain the problem and request corrected information be sent to the reporting bureau.

The reporting bureau has 30 days to respond to your written dispute. If errors are not corrected, you may need to send a second dispute to that bureau, and possibly provide additional documentation. Or, you may need to write to the underlying creditor, explain the problem and request corrected information be sent to the reporting bureau. The

The  If someone else’s debt or a stranger’s account is on your credit report, Flitter Milz can help. Whether your credit file has been mixed or mis-merged with a family member, someone with a similar name, or a total stranger, your consumer rights may have been violated.

If someone else’s debt or a stranger’s account is on your credit report, Flitter Milz can help. Whether your credit file has been mixed or mis-merged with a family member, someone with a similar name, or a total stranger, your consumer rights may have been violated.  Understand credit scores and credit reports

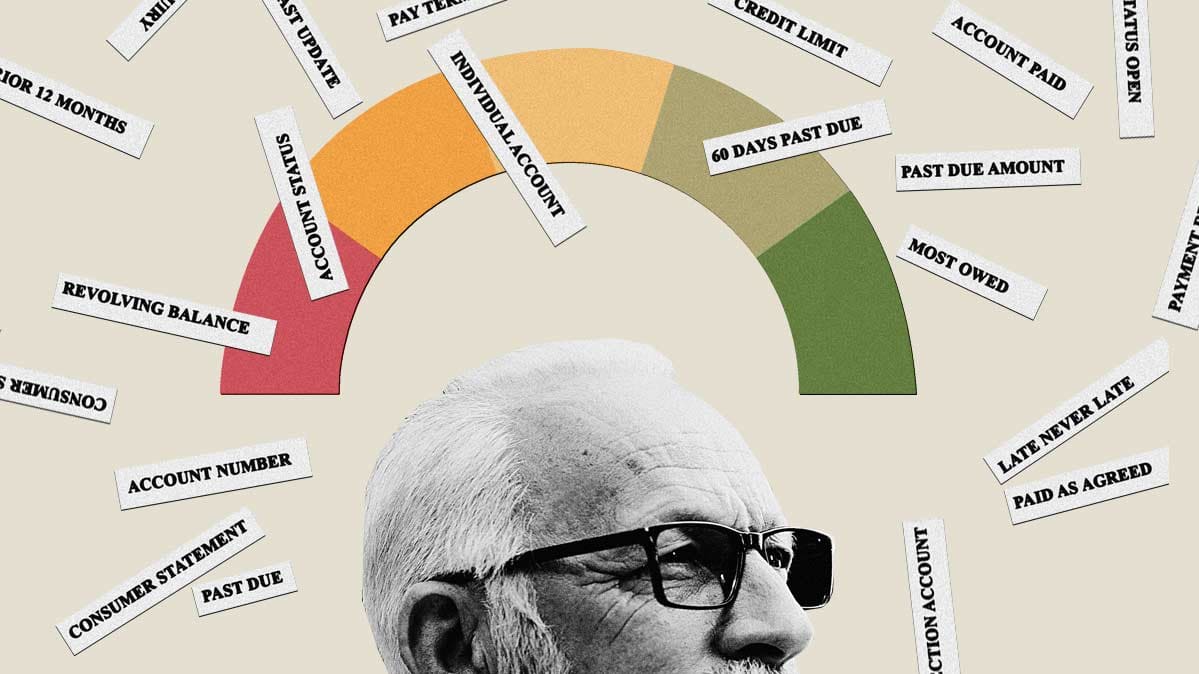

Understand credit scores and credit reports What is a credit score?

What is a credit score? credit and obtain copies of his or her credit reports and credit scores.

credit and obtain copies of his or her credit reports and credit scores. Transunion, Experian and Equifax are the three main credit reporting bureaus. These bureaus provide credit reports which list specific information about a consumer’s credit activity and payment history. Lenders use these reports to help determine whether to extend credit or not. As well, other businesses such as insurance companies and utilities, or prospective employers and landlords, may request access to a consumer’s report for use in making decisions about you.

Transunion, Experian and Equifax are the three main credit reporting bureaus. These bureaus provide credit reports which list specific information about a consumer’s credit activity and payment history. Lenders use these reports to help determine whether to extend credit or not. As well, other businesses such as insurance companies and utilities, or prospective employers and landlords, may request access to a consumer’s report for use in making decisions about you.  Do you have errors on your credit reports? Problems getting credit?

Do you have errors on your credit reports? Problems getting credit? The hard facts about Repossession.

The hard facts about Repossession. When the borrower

When the borrower  Whether or not the borrower defaulted on the terms of the auto loan, State and Federal laws govern how lenders and repo agents are to

Whether or not the borrower defaulted on the terms of the auto loan, State and Federal laws govern how lenders and repo agents are to  Send Effective Disputes

Send Effective Disputes

Attorney Andy Milz, cautions consumers that COVID-19-related payment deferrals aren’t the only problem contributing to credit reporting errors and drops in credit scores since the pandemic. He states, in this recent Consumer Reports article, that other common credit reporting errors, such as accounts or loans that have been paid off but still appear as unpaid, individual loans reported multiple times, or debt that’s listed as in collections but has been paid off, can pose hurdles, too, if you need a loan or line of credit.

Attorney Andy Milz, cautions consumers that COVID-19-related payment deferrals aren’t the only problem contributing to credit reporting errors and drops in credit scores since the pandemic. He states, in this recent Consumer Reports article, that other common credit reporting errors, such as accounts or loans that have been paid off but still appear as unpaid, individual loans reported multiple times, or debt that’s listed as in collections but has been paid off, can pose hurdles, too, if you need a loan or line of credit. Consumers are entitled to

Consumers are entitled to  If you notice errors on your credit reports, you must

If you notice errors on your credit reports, you must

An individual or business may request access to a consumer’s credit file, but they must obtain written permission from the consumer. Often, during the process of applying for credit, interviewing with a prospective employer or landlord, or applying for utilities, there may be a request to access the consumer’s credit file. Many times the credit application will serve as written permission. Other times, a specific document will be presented to the consumer for his or her signature.

An individual or business may request access to a consumer’s credit file, but they must obtain written permission from the consumer. Often, during the process of applying for credit, interviewing with a prospective employer or landlord, or applying for utilities, there may be a request to access the consumer’s credit file. Many times the credit application will serve as written permission. Other times, a specific document will be presented to the consumer for his or her signature. Consumers must

Consumers must

Being asked to co-sign a loan for a family member or close friend is a larger responsibility than most people realize. When you co-sign a loan, such as an auto loan, you and your credit are on the hook if that relative or friend decides to stop making payments on the loan. In other words, by co-signing, you are a co-borrower and must accept responsibility of terms stated in the loan agreement.

Being asked to co-sign a loan for a family member or close friend is a larger responsibility than most people realize. When you co-sign a loan, such as an auto loan, you and your credit are on the hook if that relative or friend decides to stop making payments on the loan. In other words, by co-signing, you are a co-borrower and must accept responsibility of terms stated in the loan agreement. Once the vehicle is sold, the lender may assign collection of the deficient balance to a debt collector or law firm collector. If the loan balance is not paid, the lender could choose to

Once the vehicle is sold, the lender may assign collection of the deficient balance to a debt collector or law firm collector. If the loan balance is not paid, the lender could choose to  Co-signing a loan should not be taken casually. The co-signer must consider whether or not credit may be needed for him or herself. If a co-signer has too much

Co-signing a loan should not be taken casually. The co-signer must consider whether or not credit may be needed for him or herself. If a co-signer has too much  individual the money for the purchase. In other words, you lend the individual the money and they pay you back in installments over time, or whatever agreement the two of you come up with.

individual the money for the purchase. In other words, you lend the individual the money and they pay you back in installments over time, or whatever agreement the two of you come up with.

J

J

2. Obtain Current Credit Reports. Transunion, Experian and Equifax are the three main credit reporting agencies. Consumers are entitled to receive one free credit report from each bureau every year. Sometimes, consumers choose to enroll in a credit monitoring service which enables review of credit reports on a regular basis throughout the year.

2. Obtain Current Credit Reports. Transunion, Experian and Equifax are the three main credit reporting agencies. Consumers are entitled to receive one free credit report from each bureau every year. Sometimes, consumers choose to enroll in a credit monitoring service which enables review of credit reports on a regular basis throughout the year. 4. If Inaccurate…Dispute! After obtaining your credit report, if there are errors, you should

4. If Inaccurate…Dispute! After obtaining your credit report, if there are errors, you should  One Dispute Letter Per Error. If you find multiple errors on a credit report, dispute them individually with the bureau. Enclose a copy of the credit report with the error highlighted and your supporting documents. The credit bureaus then have 30 days to respond to your dispute letter.

One Dispute Letter Per Error. If you find multiple errors on a credit report, dispute them individually with the bureau. Enclose a copy of the credit report with the error highlighted and your supporting documents. The credit bureaus then have 30 days to respond to your dispute letter. The Fair Credit Reporting Act

The Fair Credit Reporting Act  Flitter Milz, P.C. represents people in consumer credit matters related to credit reporting accuracy and privacy, abusive debt collection contact and vehicle repossessions which stem from a pending divorce or separation.

Flitter Milz, P.C. represents people in consumer credit matters related to credit reporting accuracy and privacy, abusive debt collection contact and vehicle repossessions which stem from a pending divorce or separation.

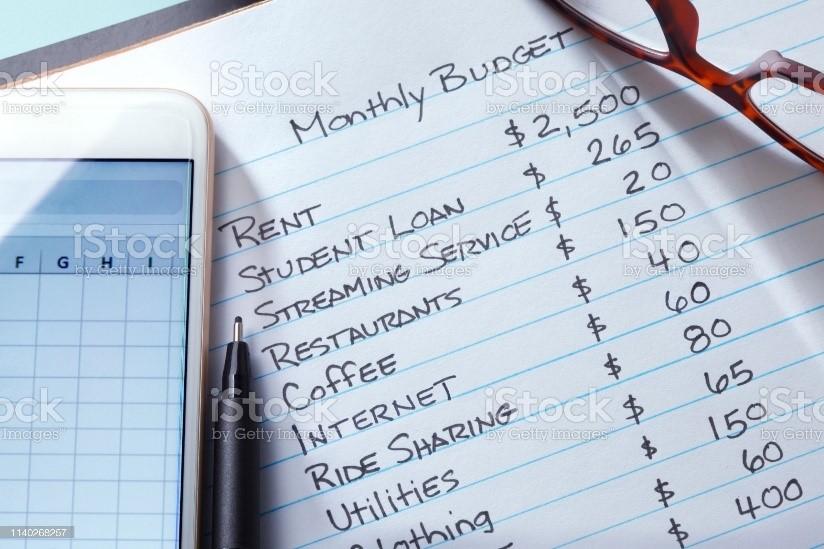

Crafting a household budget is not only necessary to help evaluate spending patterns and measure income versus expenditures, but it also helps to ensure a secure financial future.

Crafting a household budget is not only necessary to help evaluate spending patterns and measure income versus expenditures, but it also helps to ensure a secure financial future. If you know how much money is coming in versus going out each month, it becomes less likely that you’ll overspend to the point where payments are skipped or missed. Create the budget that you can stick to with a payment schedule that you can meet. When you stay in charge of your finances, you decide when it’s time to make a new purchase, whether it be for a home, education, a new vehicle, or another personal expense.

If you know how much money is coming in versus going out each month, it becomes less likely that you’ll overspend to the point where payments are skipped or missed. Create the budget that you can stick to with a payment schedule that you can meet. When you stay in charge of your finances, you decide when it’s time to make a new purchase, whether it be for a home, education, a new vehicle, or another personal expense. Flitter Milz is a nationally recognized consumer protection law firm that represents victims with consumer credit problems, such as credit reporting accuracy and privacy issues, abusive debt collection tactics, wrongful vehicle repossession, which stem from over-spending. If you have errors on your credit reports, have received contact from debt collectors, or your auto lender has repossessed your vehicle,

Flitter Milz is a nationally recognized consumer protection law firm that represents victims with consumer credit problems, such as credit reporting accuracy and privacy issues, abusive debt collection tactics, wrongful vehicle repossession, which stem from over-spending. If you have errors on your credit reports, have received contact from debt collectors, or your auto lender has repossessed your vehicle,